Charles Payne joins the recession camp.

Current indicators are not very supportive of an imminent recession:

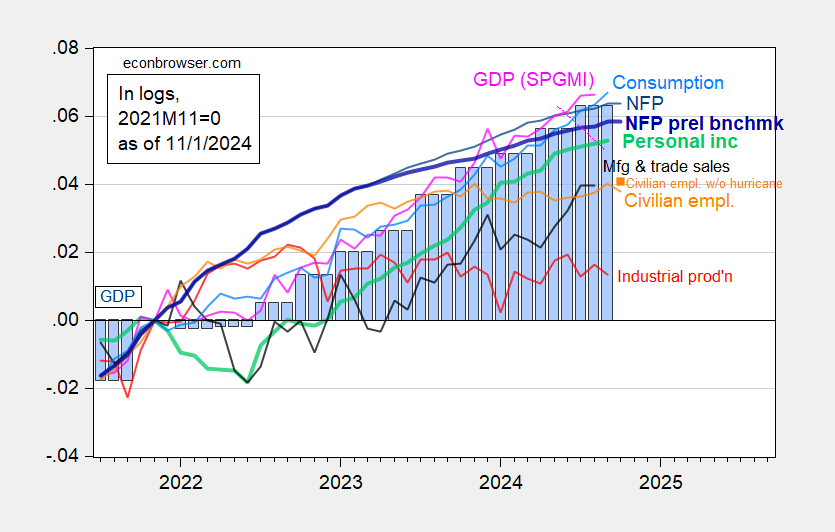

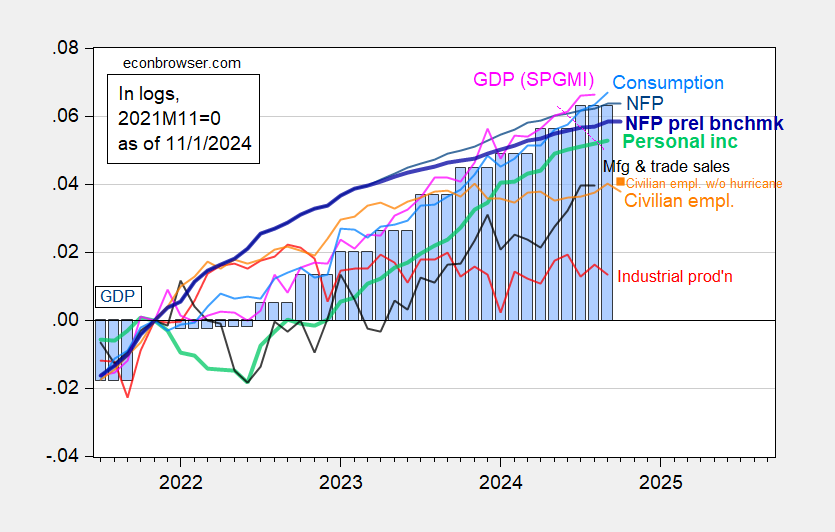

Figure 1: Nonfarm Payroll (NFP) employment from CES (blue), implied NFP from preliminary benchmark (bold blue), civilian employment (orange), civilian employment adding number of workers indicating unemployed due to weather (orange square), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold light green), manufacturing and trade sales in Ch.2017$ (black), consumption in Ch.2017$ (light blue), and monthly GDP in Ch.2017$ (pink ), GDP (blue bars), all log normalized to 2021M11=0. Source: BLS via FRED, Federal Reserve, BEA 2024Q3 1st release, S&P Global Market Insights (no Macroeconomic Advisers, IHS Markit) (11/1/2024 release), and author’s calculations.

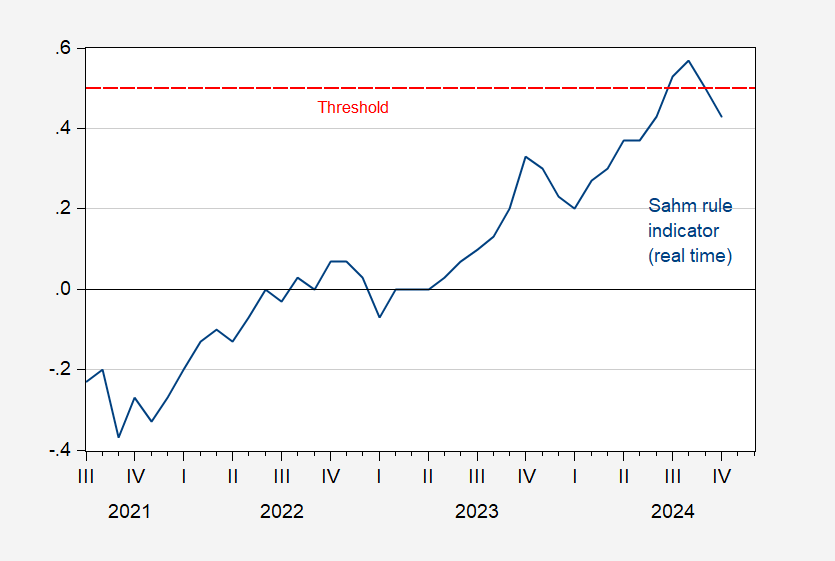

Alternative indicators show a similar story. And the Sahm rule (real time) is now below the trigger rate:

Figure 2: Sahm rule (real time) indicator, % (blue). Trigger at 0.5 ppts. Source: FRED.

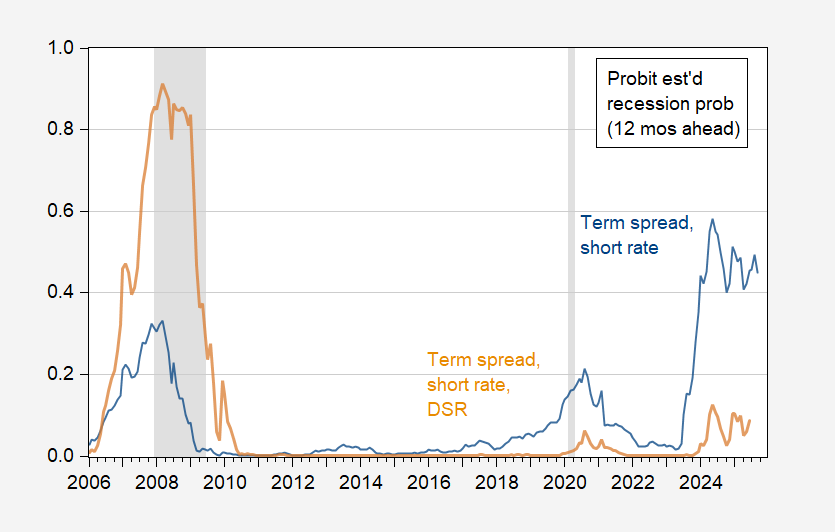

Nor is (my preferred – variation on Chinn-Ferrara (2024)) forecasting equation showing a recession soon, although a simple term spread model still signals warning (see discussion here).

Figure 3: Estimated 12 month ahead probabilities of recession, from probit regression on term spread and short rate, 1986-2024 (blue), on term spread, short rate and debt-service ratio (tan). NBER defined peak-to-trough recession dates shaded gray. Source: Treasury via FRED, BIS, NBER, and author’s calculations.