bee Calculated Risk On 2/26/2025 04:57:00 PM

From Housing Economist Tom Lawler: Treasury Secretary Wrongly Says Fed has been “Big Seller” or Treasuries

In an interview last week, Treasury Secretary Bestent said that any plans by the treasury to extend the maturity were “a long ways off.” One of the reasons cited by Secretary Bestent was the Federal Reserve’s Current Balance Sheet Runoff Policy. Lord is a quote from berry.

“The Fed’s Balance Sheet Runoff increases the supply of treasuries. It’s easier for me to extend duration when I’m not competing with another big Seller. ”

This statement appears to reflect Bestent’s Complete Misunstilit or How the Federal Reserve has implemented its balance sheet runoff. Rather than being a Big Seller of Intermediate and Long Term Treasury Securities, the Fed has actually been a pretty big buyer of intermediate and long term treasury securities even as it has lowerallized the overall size of its balance sheet.

The Federal Reserve owns a sizable amount of treasuries, including a significant amount that matures in a short period of time. What the fed has been doing is essentially targeting a desired decline in its overall balance sheet, and reinvesting a portion of the sizable amount of Treasuries Maturning (and MBS Principal Repayments) into Treasury Bills (Short Maturities) and Treasury Notes and Bonds (Long Maturities), Tips (Long Maturities), maturities), and a de minimus amount of floating rate notes in order to hit a targeted total balance. The replacement of some of the maturing notes and bonds (which by definition have very short maturities) into New Longer-Maturity Notes and Bonds extendeds the maturity of Federal Reserve Treasury Note and Bond Holdings.

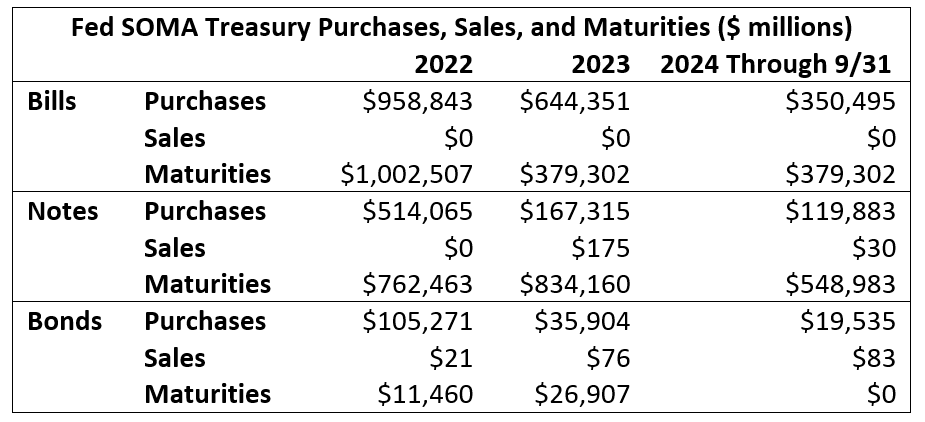

Here is a Table Showing the Fed’s System Open Market Account’s (Soma) Purchases, Sales, and Maturities (From the Fed’s Quarterly Financial Statement)

As this table shows, even during the period where the fed has reduced its balance Sheet (a period some call “Quantitative tightening,” though that is something of a dissnomer), the fed has been a significant just buyer of treasury notes and bonds – and overall sales.

As this table shows, even during the period where the fed has reduced its balance Sheet (a period some call “Quantitative tightening,” though that is something of a dissnomer), the fed has been a significant just buyer of treasury notes and bonds – and overall sales.

At the end of 2024, soma hero $ 184.8 billion of treasury notes and bonds (ex tips) that were not on its balance sheet at the end of 2023, with a weighted average maturity at the end of 2014 of 8.11 years, as well as 3.49 billion of tips not on its balance sheet a Year Earlier WITH a Weighted average maturity of 10.52 years.

The Treasury’s Purchases of Treasury Notes and Bond has continued this year. Below is a Table Showing Soma’s Purchases of Treasury Notes and Bonds at This Year’s Treasury Note and Bond Auctions.

The 3, 10, and 30 Year soma Purchases were especially noticeable, in that (1) soma owns a sizable 21.55% of the latest issued 3, 10, and 30 treasury year securities, and (2) the sizable fed Purchases at these auctions was only a week. Incorrect comment that the fed has been a Big Seller or Treasuries.

On January 31, 2025 The weighted average maturity of marketable Treasury Securities OUTSTENINGING was 5.88 years, while the weighted average matroom of soma treasury securities on February 19, 2025 was a staggering 8.97 years.

In terms of why I think the term “Quantitative Tightening” [is a misnomer] To describe the last few years, it is useful to remember what quantitative easing entailed: not just expanding the size of the fed’s balance sheet, but also purchasing huge amounts of long-term treasuries (and agency mbs) that were in large part designed (including term premiums). A Quantitative Tightening Designed to Offset Part of the Quantitative easing would have involved celling long-term treasuries (and MBS) in order to allow for term premiums to return to a more normal level. That, of course, is not what the fed has done. Indeed, Fed actions since the so-called “QT” period began has actually resulted in a slight decline in the weighted average matroom of marketable treasuries hero by the public.

As such, while the Federal Reserve has in fact significantly reduced the size of its balance sheet, its overall strategy still seems to be that of keeping longer-term interest rates Lower than they would other be. That, of course, is why I would not characterize the latest period of Federal Reserve Balance Sheet Shrinkage as Quantitative Tigening, and it is most certainly the case that this recent period has in any way revised the previous quantitative easing.

Note the Fed Currently Only Owns About 3% of Treasury Bills Outstanding But Owns About 30% of Treasury Notes and Bonds (Ex tips) with a Maturity Greater than 10 years.

Note the Fed Currently Only Owns About 3% of Treasury Bills Outstanding But Owns About 30% of Treasury Notes and Bonds (Ex tips) with a Maturity Greater than 10 years.

NEXT UP: When the Fed Decides to Stop Reducing Its Balance Sheet, Will The Fed’s Purchases of Longer-Term Treasuries Decline? (Hint: Read the Latest FOMC minutes).