at Calculated Risk on 12/12/2024 10:14:00 AM

The FDIC released the Quarterly Banking Profile for Q3 2024:

The Industry’s Net Income Decreased From the Prior Quarter, Driven by One-Time Items

Third quarter net income for the 4,517 FDIC-insured commercial banks and savings institutions decreased $6.2 billion (8.6 percent) from the prior quarter to $65.4 billion. The quarterly decrease in net income was largely driven by the absence of about $10 billion in one-time gains on equity security transactions reported in the previous quarter. The absence of these non-recurring gains was partially offset by strong net interest income in the third quarter.

…

Asset Quality Metrics Remain Generally Favorable, Although Weakness in Certain Portfolios Persists

The past-due and non-accrual (PDNA) loan ratio increased 6 basis points from the previous quarter to 1.54 percent. This ratio was 18 basis points higher than the year-earlier quarter but below the pre-pandemic average of 1.94 percent.2 Quarterly, banks reported an increase in the PDNA ratio in credit card loan portfolios (up 20 basis points to 3.36 percent), nonfarm nonresidential commercial real estate (CRE) loan portfolios (up 7 basis points to 1.69 percent), 1–4 family residential loan portfolios (up 3 basis points to 1.83 percent), and auto loan portfolios (up 5 basis points to 3.13 percent). Annually, the industry reported the largest PDNA increases in nonfarm nonresidential CRE loan portfolios (up 43 basis points to 1.69 percent), credit card loan portfolios (up 27 basis points to 3.36 percent), and commercial and industrial loan portfolios (up 20 basis points to 1.17 percent).The industry’s net charge-off ratio decreased 1 basis point to 0.67 percent from the prior quarter but was 16 basis points higher than the year-earlier quarter. This ratio was also 19 basis points above the pre-pandemic average and remained the highest quarterly ratio reported by the industry since second quarter 2013. Credit card and nonfarm nonresidential CRE loan charge-offs drove the quarterly decrease in the net charge-off ratio, which was partially offset by an increase in commercial and industrial loan charge-offs. The credit card net charge-off ratio was 4.48 percent in the third quarter, down 34 basis points quarter over quarter but still 100 basis points higher than the pre-pandemic average. The net charge-off ratio for nonfarm nonresidential CRE loans decreased 9 basis points quarter over quarter to 0.29 percent but was 25 basis points higher than the pre-pandemic average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.

From the FDIC:

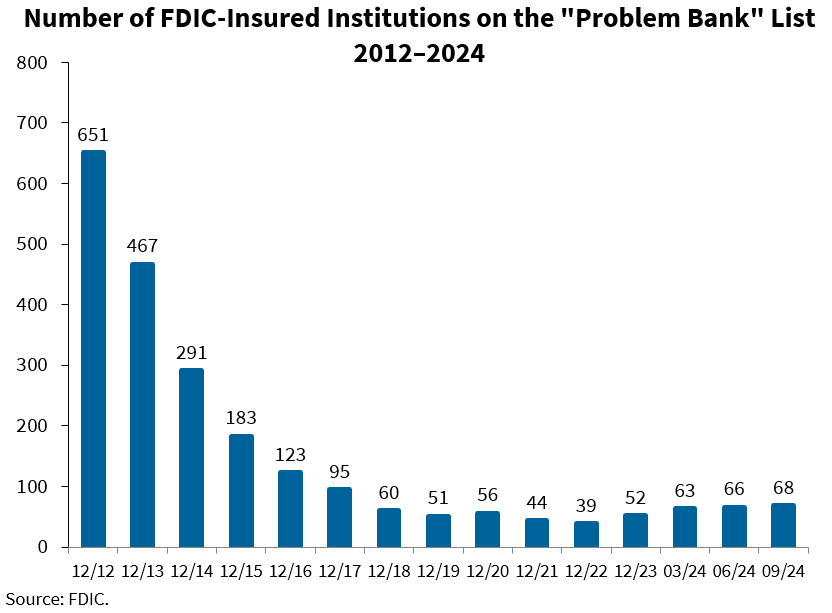

The Number of Problem Banks Increased

The number of banks on the FDIC’s “Problem Bank List” increased from 66 to 68. Total assets held by problem banks rose $3.9 billion to $87.3 billion. Problem banks represent 1.5 percent of total banks, which is within the normal range of 1 to 2 percent of all banks during non-crisis periods.

This graph from the FDIC shows the number of problem banks.